Healthcare & Medical Devices

3 major trends fueling global medical tourism market size

Global medical tourism market size is slated to witness an exponential growth owing to higher prevalence of chronic diseases among people of all ages, along with excessive rising healthcare costs in developed nations. Nowadays, emerging economies such as India, Thailand, and Brazil have increasingly become a favored destination for medical tourists.

Essentially, these countries provide health care services with cutting-edge technology comparable to the advanced treatments offered worldwide, besides offering same quality treatments at more affordable price. Cost-effective treatment options and personalized care will become significant drivers expanding medical tourism market outlook.

Described below are some notable factors projected to impact the growth of medical tourism over the next few years:

Rising prevalence of cardiovascular disease in North America

According to reports, cardiovascular disease has become an underlying cause of death in the United States. Nearly 47% Americans exhibit at least one key risk factor for heart disease, such as diabetes, obesity, blood pressure, among others. However, high level of expertise and low treatment costs in developing countries have become an attractive option for foreigners who need surgeries, without much strain on their pocket.

Modern hospitals, advanced treatments, and proficient doctors in Asian countries are becoming lucrative choices for cost-effective medical treatment, which boosts the economy of a country and inadvertently fuels the development of healthcare services.

In terms of technological intervention, many big hospital chains and medical equipment providers in developing nations are contributing towards newest innovations in terms of addressing cardiovascular diseases, like the introduction of AI-powered cardiovascular disease risk score API by Apollo Hospitals, in association with Microsoft, to predict the risk of cardiovascular disease among people.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/3022

Adopting innovative developments into healthcare services will influence more medical tourists to visit other countries for affordable treatments, without compromising on quality, which will proliferate medical tourism market size over the coming years.

Consumption of medical treatments and procedures in India

Medical tourism has become a key growth sector for India as healthcare segment in the country excels in using the most advanced technologies on par with nations like the U.S. and has numerous accredited healthcare providers. With the rising trend of tourists for medical treatments, many companies are bringing out more simplified and easier options for them by offering complete packages inclusive of high-quality treatment, traveling cost and ease of communication.

Expatriates living in North America and Europe, still having family connections in India, increasingly prefer to travel to the country for heart and other crucial surgeries. Reports suggest that India medical tourism market will bring significant opportunities with a profitable 11.3% growth rate through 2025.

In March 2019, India and the Africa union had signed an MoU to strengthen the cooperation in healthcare sector. The MoU will bring cooperation in the areas of capacity building, research and development, health services, pharmaceutical trade and manufacturing capabilities for drugs and diagnostics. Such initiatives will bolster global health research and address regional needs, creating remarkable prospects for medical tourism industry.

Increased demand for affordable cosmetic surgeries

According to American Society of Plastic Surgeons, in 2018 around 18 million people underwent surgical and minimally invasive cosmetic procedures in the U.S. With a surge in the number of cosmetic procedures and plastic surgeries, cosmetic surgery practitioners in countries like Brazil and Thailand are offering all kinds of procedures at comparatively cheaper rates.

Number of cosmetic transformations and plastic surgeries such as eyelid surgery, tummy tucks, breast augmentation, among others are continuing to increase in developed nations, but high costs are driving people towards lower economy markets. With the spread of social media platforms and increased image consciousness among women, aesthetic enhancements have become a common trend.

It has been observed at cosmetic procedures among men has also increased at a faster pace over the last few years, which will provide significant consumer base for medical tourism market players.

Consistent R&D efforts, innovations, and cost-effective treatments will help fuel the demand for surgeries in developing countries. Key players in medical tourism industry include Max Healthcare, Manipal Hospitals, Narayana Health, Mount Elizabeth Hospitals, KPJ Healthcare Berhad, Raffles Medical Group, among several others.

According to a latest research study by Global Market Insights, Inc., global medical tourism market is anticipated to be worth more than USD 30 billion by 2025.

Author Name : Deeksha Pant

Rising prevalence of chronic health conditions will fuel patient monitoring devices market size

Rise in the number of patients suffering from critical diseases coupled with rapidly advancing technology will drive patient monitoring devices market size over the next few years. Monitoring devices accurately collect and display physiology data on a real-time basis, which is important for the doctors to take immediate and precise course of action. A surge in cardiac disorder patients and increased disposable incomes will push the demand for heart monitoring devices and expand the scope of medical technology sector.

Evolving digital technologies powering monitoring devices have influenced the operational costs and made them more effective. They have also reduced the need of hiring a permanent skilled staff member to interpret data for the customers. According to a research in University in Chicago, use of continuous glucose monitors (CGM) is extremely cost effective for adult patients suffering from Type 1 diabetes compared to just using test strips daily. The devices reportedly improve glucose control and result in reduced low blood sugar incidents, endorsing the products offered by patient monitoring devices industry players.

Increasing prevalence of heart diseases among patients around the world will help bolster the demand for patient monitoring techniques. According to the American Heart Association (AHA), arrhythmias affect over 4 million patients in the U.S every year. In order to record and interpret the electrical activity of the heart, electrocardiography (ECG) is widely used in the hospitals to detect abnormal heart rhythms. The status of ECG machines have changed over time with the device moving to non-cardiology departments like electrophysiology labs, nursing and emergency departments as well as for respiratory therapy.

Several government initiatives across different countries will influence patient monitoring devices market outlook over the projected timeframe. For instance, India had introduced the Make in India campaign a few years back to bring in large number of investments into manufacturing and research sector. Investments are also being made into the healthcare segment, which will help boost the production and use of medical devices, including patient monitoring devices. A fast-growing startup space in the country, stimulated by the influx of capital, will encourage added research and development efforts towards building advanced healthcare technologies.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/4069

Wireless patient monitoring devices market is slated to register a CAGR of 5% over the forecast period, as the products help physicians examine several patients simultaneously and remotely. A professor at the Massachusetts Institute of Technology has developed a device called Emerald that analyzes the surrounding radio signals via machine learning algorithms. The device can extract several physiological metrics that are related to mobility, sleep stages, breathing, sleep apnea, gait and others. The innovation undoubtedly represents a widespread scope for monitoring devices in healthcare.

Development of wireless medical devices can apparently reduce the number of patients needed during clinical studies and shorten the lengths of trials involved. Moreover, it could help in reducing the repeated clinical site visits, lowering the direct costs to different pharma companies as well as the indirect cost that accrues owing to the recruitment difficulties, besides the expenditure on subject site visits. Substantial benefits offered for clinical stage companies and research facilities will lead to escalating adoption of such devices and propel patient monitoring devices industry share considerably.

Growing number of patients with acute diseases and a dramatic rise in the number of road accidents that require critical surgeries have increased the demand for anesthesia monitors. Anesthesia monitors are used during surgery to the track the vital signs of the patients like temperature and blood pressure while they are heavily sedated. Augmented deployment of anesthesia monitors in hospitals and ambulatory surgical centers will significantly thrust global patients monitoring devices market size.

According to the reports by the U.S. Centers for Disease Control & Prevention, chronic diseases account for close to 75% of the entire healthcare expenditure. Amongst the most prevalent diseases, chronic disorders are the costliest health conditions with over 45% of Americans suffering from various diseases in this category. Hospitals offer major benefits for the treatment of such diseases with the help of patient monitoring devices. With a large volume of patients every year needing surgeries and having continuous treatment regimens, U.S. patients monitoring devices industry will witness an exponential growth.

Change in lifestyle, increased consumption of junk food and lack of physical exercise has increased the occurrence of serious health conditions in North America, like endocrine disorders, high cholesterol levels and cardiovascular diseases. The region will prove to be a lucrative target market for monitoring device manufacturers due to a massive healthcare expenditure and favorable health insurance policies. In fact, North America patient monitoring devices industry size is slated to grow by more than 4% over the project years.

Expanding geriatric population, who prefer remote patient monitoring devices owing to general convenience, will help proliferate the advanced healthcare sector in the coming years. Key market players involved in supplying vital patient monitoring products are IBM, Phillips Healthcare, GE Healthcare Limited, OSI Systems and Honeywell Lifecare Solutions, among others. Increased convenience in deploying IoT technologies will fuel global patient monitoring devices market, which is anticipated to reach annual revenues of over USD 27 billion by 2025.

Author Name : Riya Yadav

Veterinary imaging market outlook to observe a strong transformation via rising adoption of small companion animals

Increasing instances of pet adoption and the subsequent expansion of pet insurance sector is expected to propel global veterinary imaging market growth over the forthcoming years. Improving economic conditions, increasing spending power, and growing social awareness regarding adoption of domestic animals have created ideal growth conditions for the veterinary imaging industry.

With growing pet adoption, the global pet insurance industry has witnessed a substantial boost in recent years. First introduced in Sweden, where 50% of the pet population is insured today, the pet insurance sector is slated to augment growth of the veterinary industry. Making expensive pet healthcare procedures, including veterinary imaging services, accessible to more pet owners would propel veterinary imaging market share further.

Veterinary imaging is a non-invasive diagnostic procedure that makes medical images of animals’ bodies to diagnose diseases. In today’s age where companion animals are increasingly susceptible to a plethora of ailments, the procedure has become integral – specifically, for small animal internal medicine and oncology, to plan out sophisticated treatments.

The American Veterinary Medical Association estimates that one in four dogs develop neoplasia at some point in their lives. In fact, approximately 50% of the dogs that are aged above 10 years are highly likely to develop cancer. Meanwhile, when it comes to the world’s second most common pet; cats, there is far led information regarding their susceptibility to serious diseases. However, data suggests that some types of cancer, like lymphoma, are highly common in cats.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/4067

Attributing to the commonplace nature of such serious ailments and the integrality of veterinary imaging procedure in creating a competent treatment plan, demand for veterinary imaging is bound to go up over the forthcoming years.

The pet owning trend has grown at such a massive scale globally that it is successfully bringing in revenue growth from developing economies. According to estimates, India’s companion pet population reached 10 million in 2014. The country is considered to be the fastest growing global pet industry in the world.

This rapid growth in pet ownership is calling for the launch of an organized pet healthcare service providers across India. This demand when coupled with upcoming insurance policies would be able to facilitate seamless comprehensive solutions to the pet owners. Expanding capabilities of the pet healthcare and pet insurance industry in India are expected to pave the way for the veterinary imaging market outlook during the forecast timeframe.

From a regional perspective, North America has covered substantial contribution of veterinary imaging market share in the past years. The region is expected to register a significant growth over the forecast period primarily due to surging healthcare spending on the improvement of animal management.

The companion animal adoption trend throughout these regions has remained strong over the years, showcasing a steady growth rate. In fact, according to American Pet Products Association, the number of U.S. households with a pet reached the 84.6 million with an estimated number of pet cats and dogs registered at 183.9 million between 2017-18.

North America also boasts of a highly sophisticated pet healthcare infrastructure along with a well-established pet insurance industry, whose combined gross written premiums reached $1.2 billion in 2017, according to The North American Pet Health Insurance Association (NAPHIA). Such pre-established amenities, while making access to veterinary services significantly easier, also augment growth of the region’s veterinary imaging market trends.

All in all, owing to growing instances of companion animal adoption in emerging economies and North America’s strong pet adoption culture, demand for veterinary imaging procedures is slated to rise substantially during the forecast time period. Growing awareness among the people about the benefits of healthcare insurance facilities will also improve the product demand over the years ahead. In fact, a research report by Global Market Insights, Inc., estimates that veterinary imaging market size would cross a valuation of $2 billion by 2025.

Author Name : Akshay Kedari

High prevalence of obesity in the U.S. and India to drive anti-snoring treatment market by 2025

Anti-snoring treatment market share is anticipated to be driven by growing incidence of obesity which leads to snoring and rising awareness about the health implications of snoring. Medical equipment companies are developing non-surgical anti-snoring devices which are capable of treating snoring issues in patients. Indolent and alcoholic lifestyle of people around the globe has been driving the occurrence of snoring, which will fuel the industry trends over the forecast period.

One of the most important risk factors causing snoring among the elderly population is obesity. Consumption of unhealthy diet and alcohol, changing lifestyle habits, insufficient physical exercise, and smoking has augmented obese population globally. Overall, about 13% of the world’s adult population were obese in 2016. In the same year, over 1.9 billion adults aged above 17 years were noted to be overweight, out of which more than 650 million were obese. The incidences of obesity globally compounded by three times between 1975 and 2016.

Factors such as increased consumption of energy-dense foods which are high in fat and decline in physical activity due to the sedentary nature of many forms of work and increasing urbanization has led to such trends observed in obesity which in turn has augmented anti-snoring treatment market size as obesity is closely related to snoring.

Obesity in United States has been noted to be a serious health issues. In 2015-2016, obesity incidence among children and adolescents was recorded at 18.5% and affected about 13.7 million. The prevalence of obesity among adults in the same timeframe was 39.8% and affected about 93.3 million.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/3998

The lifestyles of the people in the U.S. has given rise to obesity which is one of the key causes of snoring. Rapid growth in snoring problems can be accredited to augmenting obesity among the aged population and rising adoption of a sedentary lifestyle. Approximately 90 million adults endure snoring problem in the U.S. and need anti-snoring therapy. Growing demand of anti-snoring treatments and technological advancements of medical devices in the nation is likely to add growth impetus to anti-snoring treatment industry outlook. U.S. anti-snoring treatment market size surpassed $5.6 billion in the year 2018 and is expected to grow at dynamic pace over 2019-2025.

Besides the U.S., India has the second highest number of obese children in the world, with 14.4 million reported cases. The proportion of overweight or obese women (15-49) increased from 13 to 21 percent, and from 9 to 19 percent for men. In addition, there has been an increase in the mean BMI from 20.5 in 2005-06 to 21.9 in 2015-16 raising snoring concerns in the country. A huge number of untreated people with a snoring disorder will offer lucrative scope for anti-snoring industry growth in the country. Indian anti-snoring treatment market is projected to grow at 4.0 percent CAGR over 2019-2025.

One of the reasons leading to increased rate of obesity and snoring is alcohol consumption. In the U.S., one in six adults binge on drinks around four times a month, consuming about seven drinks per binge. Over 90 percent of adult drinkers report binge drinking in the past 30 days. Surge in prevalence of alcohol consumption has significantly given rise to obesity and simultaneously to snoring which will supplement anti-snoring treatment market.

Technological advancements in anti-snoring treatments have been on the rise and medical devices firms are coming up with various new therapies which will enhance their revenue share. For instance, Apnea Sciences Corporation recently launched SnoreRx, a non-surgical anti-snoring device. FDA has sanctioned SnoreRx to be denoted as the first and only oral appliance for treatment of snoring sans prescription. Upsurge in innovations and adoption of advanced anti-snoring devices will encourage increased production and contribute to anti-snoring treatment market growth.

According to report by ResMed, in 2018, 936 million people worldwide had sleep apnea. Recently, ResMed announced that it has acquired HB Healthcare (HBH) to help millions of South Koreans with sleep apnea, chronic obstructive pulmonary disorder (COPD) and other respiratory conditions. One in five Korean adults is believed to have sleep apnea and the company’s effort to offer therapy to the people there will substantially help increase anti-snoring treatment industry share.

Several anti-snoring treatment industry majors are adopting various strategic alliances such as mergers and acquisitions, partnerships and strategic collaborations with other contributors to considerably increase revenue shares and expand anti-snoring treatment market size. Global Market Insights estimates anti-snoring treatment market size to exceed $18 billion by 2025.

Author Name : Anchal Solanki

Rising health concerns among pet animals to foster veterinary surgical instruments market size

Increasing adoption of pet animals around the world will fuel the demand for animal surgeries, in turn driving veterinary surgical instruments market outlook over the forecast period. According to a National Pet Owner Survey which the American Pet Products Association (APPA) conducted in 2017-18, 68% of households, or about 85 million families in the United States own a pet. This is much higher compared to 56% of households in the U.S. back in 1988, the first time that this survey had been conducted.

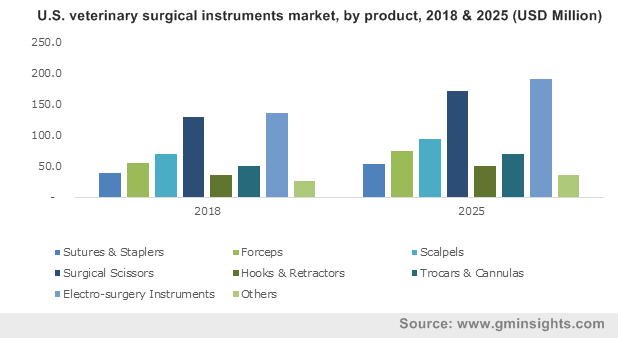

U.S. veterinary surgical instruments market, by product, 2018 & 2025 (USD Million)

The dramatic increase in the number of veterinary hospitals around the world along with the rising choice to follow veterinary practices will boost veterinary surgical instruments industry size. According to the reports by AVMA in 2017, veterinary practices ranged from 28,000 to 32,000 with a total number of 1, 10,531 veterinarians present in the U.S. Rise in the number of these practices and surgeons will create a need for the use of various surgical equipment to perform different kinds of procedures on pet and farm animals.

Periodontal disease is among the most common diseases in pets like cats and dogs that once turn 3 years old, start witnessing symptoms of the disorder. The disease can be critical and can affect theliver, kidney and heart muscles. The need for surgeries for treating animals experiencing the disorder or its outcomes will propel veterinary surgical instruments market trends significantly. The dental surgery segment accounted for a massive USD 397.1 million in the year 2018 and will show consistent growth in the forthcoming years.

Orthopedic surgeries have been on the rise among animals owing to automobile accidents or general security concerns, when dogs may be needed for security purposes are exposed to armed robbers and burglars. The Veterinary Teaching Hospital in the University of Ibadan in Nigeria produced a study wherein the results of the orthopedic cases were 16.7%, that is 127 out of 618 small animal surgeries that took place. The cases for fractures were the highest with 61.42% and hip dysplasia accounted for around 14.17% of the procedures. Such numbers indicate the possible surge in demand for orthopedic procedures in the future, reinforcing veterinary surgical instruments industry size.

Electrosurgery is expected to grow in the forthcoming years owing to its high frequency and easy to use properties. The high rate of accuracy along with the reduction in the tissue damage while operating will contribute to its demand. Electrosurgery has large number of applications in several surgical procedures and is highly precise with its functioning that will propel adoption among veterinary surgeons globally. Advancements in the production of these equipment will certainly help boost industry-wide expansion and offer new prospects to surgical instrument manufacturers.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/3700

The proliferation of government organizations related to animal healthcare and even separate animal healthcare organizations will increase the demand for treatments from large animals segment across developing nations. Large animals can usually suffer from chronic diseases and the prevalence of bone diseases in animals staying in farms will drive the growth of veterinary surgical instruments market share. These organizations focus on animals in zoos and sanctuaries along with the ones on the verge of extinction.

Soaring demand for pet insurance taken by owners has been strengthening the U.S. veterinary surgical instruments market, which is anticipated to surpass USD 668.5 billion in valuation by 2025, due to consistent adoption of pets in the country. Collective efforts put by the major key market players will help bolster the consumption for veterinary surgical instruments in the U.S. According to NAPHIA (North American Pet Health Insurance Association), the sum of pets that have been insured in the United States had reached 2.1 million in the year 2017.

Several market players like B. Braun, Ethicon, Medtronic, STERIS Corporation, Sklar Surgical Instruments, Surgical Direct, Smiths Group and World Precision Instruments have constantly been involved in the development and distribution of critical equipment. They are consistently involved in strategic collaborations with hospitals and professionals to capture higher market share than other companies. Global veterinary surgical instruments market size is projected to surpass USD 1.8 billion by 2025.

Author Name : Mateen Dalal

Surge in infertility rates worldwide to boost in-vitro fertilization services market size by 2025

Rising cases of infertility among women & stress induced by fast paced urban lifestyle is driving in-vitro fertilization services market share. According to the Center for Disease Control and Prevention (CDC), around 6.1 million women in the U.S., aged between 15-44 years, have difficulty getting or staying pregnant. Surge in infertility cases among women can be attributed to factors like hormonal imbalance, excess alcohol & caffeine consumption, eating disorder, obesity and stress.

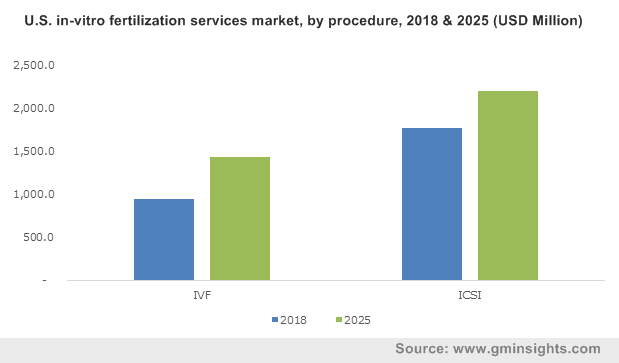

U.S. in-vitro fertilization services market, by procedure, 2018 & 2025 (USD Million)

Additionally, growing trend of delaying pregnancy until the ages of 30 to 40 is also leading to rise in cases of infertility lately. For instance, according to The Office on Women’s Health (OWH), woman over the age of 30 are often diagnosed with fertility problems.

Rising obesity as well as hectic urban lifestyle will boost in-vitro fertilization (IVF) services market trends over the forecast period. Furthermore, supportive government initiatives to promote such procedures will positively impact industry forecast. Citing an instance, as of April 2019, female employees in Romania, who decide to undergo an in-vitro procedure, will be offered three days of paid leave owing to recent changes in the country’s Labour Code which aims at promoting in-vitro fertilization.

Additionally, in July 2019, the French government passed a bioethics bill that would allow in-vitro fertilization (IVF) for single women and lesbian couples in the country. Such advancements are expected to offer growth opportunities for players in the in-vitro fertilization services market.

With growing infertility rate among men worldwide, the intracytoplasmic sperm injection (ICSI) procedure segment is anticipated to generate added proceeds in the coming years. According to a new study from the Hebrew University of Jerusalem, sperm count in men from Europe, North America, Australia and New Zealand has declined by 50%-60% between 1973 and 2011. Moreover, experts suggest that men across these regions are likely to have little or almost no reproductive capacity by 2060.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/3441

Reportedly, factors like unhealthy lifestyle, lack of physical activity, work stress, pollution, poor diet, alcohol consumption and smoking contribute to increased rate of infertility in men. Doctors from the All India Institute of Medical Sciences (AIIMS) have also reported that over 12–18 million couples in India are diagnosed with infertility each year.

With rapid medical advancements and development in assisted reproduction techniques like intracytoplasmic sperm injection (ICSI) and IMSI (intracytoplasmic morphologically selected sperm injection), men with poor sperm will also be able to father children. According to a study by the University of Aberdeen, among 2,133 women who undertook IVF or ICSI procedures, 1,060 had achieved a live birth, of whom 15% later had another live birth independent of treatment within five years. With such promising results, the demand for ICSI will increase significantly in coming years and is anticipated to boost IVF services industry growth over the forecast period.

Based on end-use, the fertility centers segment in IVF services market is anticipated to accrue momentous growth because of increasing demand for infertility procedures worldwide coupled with rapid advancements in reproductive technology. Increasing urbanization and rise in number of investments & infrastructure expansions worldwide will further compliment segment growth.

Additionally, in 2019, Shady Grove Fertility (SGF), one of the leading fertility centers in the U.S., announced the opening of its newest full-service in vitro fertilization (IVF) center in Tampa, Florida, providing access of high-quality fertility care to patients. Expansions like these will offer new growth opportunities in the fertility centers segment, thereby boosting IVF services market size.

In terms of regional share, the U.S. IVF services market is anticipated to hold major revenue share due to growing awareness regarding IVF procedures along with rise in government initiatives to encourage people to avail such treatments. In 2016, Congress authorized the Department of Veterans Affairs to cover IVF and other fertility treatments for veterans who struggle to have children caused by service-related issues. Additionally, increasing prevalence of infertility among Americans will further boost U.S. IVF services market size over the forecast period.

Global IVF service market will reap the results of rapid advancements in reproductive technologies and rising cases of infertility worldwide. Increasing investments in R&D and expansion strategies are supplementing fertility center growth worldwide. Additionally, government initiatives focused on lowering IVF treatment cost is enhancing industry outlook. Global Market Insights, Inc., estimates IVF services market size to exceed USD 17.3 billion by 2025.

Author Name : Mateen Dalal

Rising CVD prevalence to accelerate stent market share

Robust globalization and urbanization trends that have led to unhealthy meal consumption habits are driving stent market size. Stents are used mainly in surgeries pertaining to heart disorders that have been increasing in the last few years due to modern, sedentary lifestyles, unhealthy dietary patterns, rise in mental stress, growing consumption of processed foods, and mounting air & water pollution.

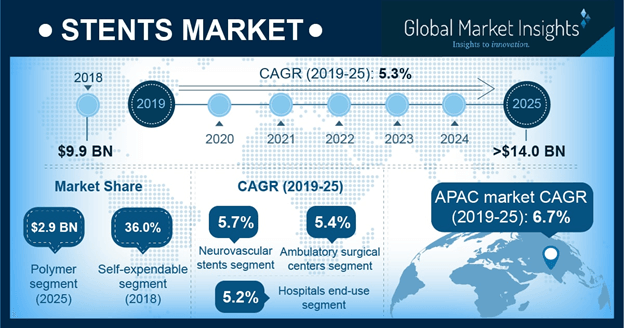

U.S. Stent Market, By Type, 2018 & 2025 (USD Million)

Changing consumer lifestyles have led to rising prevalence of health hazards like obesity, depression, hypertension, and diabetes which are major risk factors accelerating cardiovascular diseases (CVDs). The surging prevalence of CVDs will drive global stent industry share.

As per statistics by the World Health Organization (WHO), more than 75% deaths due to CVDs occur in low-income and middle-income countries and 31% of all deaths worldwide occur because of CVDs. More precisely, four out of five CVD deaths are because of strokes and heart attacks. Identifying the high risk of mortality associated with CVDs, regulatory organizations and leading pharmaceutical companies are putting in their efforts to prevent premature deaths by providing technologically advanced medical devices which will drive stent market size.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/3372

As per estimates by WHO, the prevalence of CVDs is projected to grow by 50% between 2010 to 2030 in China mainly due to rising number of patients with obesity, diabetes, and blood pressure. Considering the fact that China accounts for a population of more than 1.36 billion in 2014, there are huge business opportunities for stent market leaders in the nation.

China’s one-child policy and other stringent norms will increase the geriatric population in the country. The dramatic imbalance between young and aged people may generate more number of health hazards related to CVDs since the elderly are susceptible to such disorders. This trend will further stimulate stent market size. Global Market Insights, Inc., predicts that rise in the elderly population worldwide will augment worldwide stent industry share that will cross more than USD 16 billion by 2025.

Developing and underdeveloped countries will turn out to be game-changers in stent market owing to the prevalence of unhealthy eating habits, consumption of tobacco, lesser physical activities, and sedentary livelihood. WHO analyzes that increasing risk associated with heart related disorders will not only boost the need of technological advancement in the healthcare sector but will generate awareness among the masses. Growing prevalence of CVDs will thus enhance not only stent market but will drive worldwide cardiovascular ultrasound market over the coming years.

The U.S. stent market size will grow significantly over the forecast period. The growth will be driven by the rising demand for minimally invasive medical devices. As per estimates, U.S. held over 30% of the market share in 2018 and may dominate the global stent industry over the coming years. The presence of supportive reimbursement policies and extensive healthcare expenditure will drive the regional growth by 2025.

Stent market is sometimes constrained by the exorbitant product price, though efforts are being made to tackle the pricing trends. For example, in India, since 2018, prices of stents are fixed by the government. It resulted into 85% decrease in the price of stents. As per the data shared by the National Pharmaceutical Pricing Authority (NPPA), earlier hospitals were enjoying profit margins of 650% from each patient, which will now be curbed. Decrease in the device prices will augment India stent market trends over the coming years.

Ongoing development in the healthcare sector and increasing availability of quality products will accelerate the demand for bio-absorbable stents. Moreover, formulas used by the WHO for delivering cost-effective medical products is slated to propel the industry share over the years ahead.

Author Name : Sunil Hebbalkar

4 key trends impacting upper limb prosthetics market forecast

Upper limb prosthetics market size has experienced an exponential growth over the last couple of decades owing to rising cases of road accidents. According to the World Health Organization (WHO), nearly 20-50 million people suffer from non-fatal injuries due to road accidents, which in many cases leads to disability.

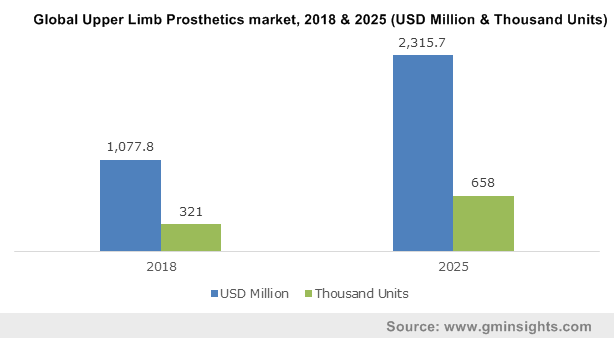

Global Upper Limb Prosthetics market, 2018 & 2025 (USD Million & Thousand Units)

Violence has become a global public health problem and violence in certain situations lead to amputations, giving rise to the need for prosthetics. Reportedly, the estimated count of new amputations range between 10,00,000 and 15,00,000 per year, globally. Advancement in technology and medical science can facilitate remarkable prosthetic attachments for patients. Steadily growing frequency of amputations is steering global upper limb prosthetics market forecast.

Research and investments in the medical device sector is leading to increased innovations in prosthetics arms. Apparently, scientists at the University of Utah have developed technologies than can provide certain degree of sensation for people with amputations. This takes place through surgical implantation of several electrodes directly next to the nerve fibers and when the interface is turned on, the patients can not only feel something but also distinguish between touching something hard or soft. Similar developments in the healthcare sector is positively influencing upper limb prosthetics industry outlook.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/4235

Various devices comprising the segment of upper limb prosthetic components include terminal devices, prosthetic wrists, prosthetic shoulders, prosthetic elbows and prosthetic sockets. Listed below are some factors expected to impact the demand for upper prosthetic limbs over the coming years:

Increased adoption of terminal devices

Terminal devices under upper limb prosthetics are witnessing steady adoption rate owing to their low maintenance. These devices can be active, where they open and close for hold items, or be passive, being used for cosmetic purposes. Cable operated terminal devices, hooks and myoelectric operated hands are few key types of terminal devices.

Terminal devices are considered to be extremely cost effective, low maintenance and additionally can be customized as per the needs of the patients. This makes them highly popular as the functionality of the device can be adjusted depending on the requirement of the patients. Undoubtedly, augmented deployment of terminal devices to meet distinct needs of consumers will provide an increased impetus to upper limb prosthetics industry size.

Growth of prosthetic clinics

Providing direct and easy access to medical care for amputations is a vital factor driving establishment of prosthetic clinics worldwide. Amputees are able to benefit from specialized treatments, physiotherapies and affordable prosthetic limbs through clinics designed to meet their every need.

Owing to features that offer enhanced safety and precision with respect to prosthetic implants, upper limbs prostate market size has expanded significantly through the robust growth of prosthetic clinics which offer comprehensive support in order to optimize the heath of the patients. Since these clinics focus only on facilitating prosthetic services, they are extremely experienced and offer complete start- to – end diagnosis under one roof.

Typically, a prosthetic clinic will provide aid with body-powered protheses, activity specific prostheses, myoelectric arms, as well as partial hand and finger prostheses. More importantly, gradual inclusion of coverage for some amount if prosthetic costs into medical insurance products will fuel the industry trends.

Increased demand in the U.S.

U.S. upper limb prosthetics market share is expected to register a steady growth rate over the coming years due to rising awareness among citizens regarding prosthetics, adoption of highly advanced medical technology and availability of skilled professionals. Constant R&D activities in the healthcare industry will benefit the overall upper limb prosthetics landscape in the country. U.S. witnesses a strong healthcare spending record, which had reportedly reached USD 3.5 trillion in the year 2017.

Patients are being made aware about innovations in prosthetics frequently and are also informed about ways in which they can regain the functioning of a lost limb prosthetically. The month of April 2019 was observed as a Limb Loss Awareness month with the aim to educate, share and celebrate living with limb difference and loss. Initiatives like these add vitality to the prosthetic techniques and will offer lucrative business opportunities for North America upper limb prosthetics industry players.

3D printing transforms prosthetic manufacturing

Increasing innovations in the medical field are translating into development of precise healthcare solutions that benefit both patients and doctors by improving outcomes and lowering costs. 3D printing provides faster execution of prototyping ideas, higher cost savings and inventive problem solving. 3D printers can seemingly recreate artificial body parts and the technology is widely being explored to build prosthetic hands, arms, legs and feet.

The e-NABLE is an online community that focuses on mechanical prostheses like wrist-actuated and elbow actuated designs which are easy to print and can be assembled by anyone. Additionally, there are certain open source communities specifically focusing on 3D printed myoelectric hands and arms, while being involved in prototyping models that can be mass-produced.

Introduction of 3D printing in the healthcare sector will undoubtedly prove to be highly beneficial for patients, facilitating intricate care along with providing customization of prosthetics in terms of color, design, form and sizes. 3D printing is also a more economical option, magnifying its impact across global upper limb prosthetics market share.

Author Name : Shreshtha Dhatrak

3 major trends impacting influenza diagnostic tests market in 2019 and beyond

Increasing prevalence of influenza is expected to provide impetus to influenza diagnostic tests market outlook over the forecast duration. The industry trends are also expected to be influenced with the growing awareness among the population about early influenza diagnosis and effective treatment gains traction.

Influenza is a viral infection that attacks the respiratory system (lungs, throat and nose) and is commonly called the flu. Influenza virus testing is important in clinical management as the results may influence clinical decisions such as whether to initiate antiviral treatment, to implement infection prevention, perform some other diagnostic testing, or take control measures for influenza.

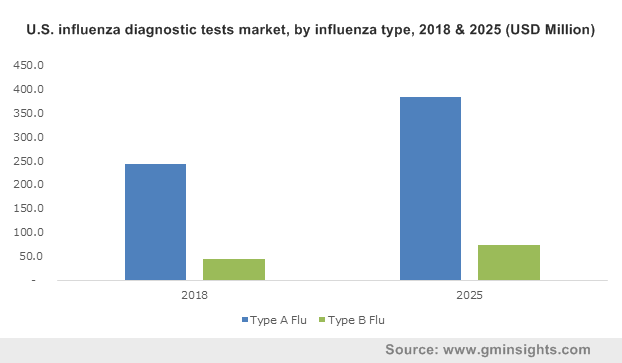

U.S. influenza diagnostic tests market, by influenza type, 2018 & 2025 (USD Million)

During respiratory illness outbreak in closed settings like hospitals, offices, long-term care facility, summer camp, schools, etc., testing for influenza virus infection can be very helpful in determining if influenza is the cause of the outbreak. Since testing for influenza virus is recommended for all patients with suspected influenza, influenza diagnostic tests industry share has received a potent boost from such tests to confirm or rule out the presence of the virus.

Symptoms of influenza can be similar to those caused by other infectious agents including respiratory syncytial viruses, parainfluenza viruses, rhinoviruses, etc. Influenza can worsen and develop complications, such as bronchitis, pneumonia, asthma flare-ups, ear infection, heart problems etc. which have created urgent need for influenza diagnostic and treatments, adding impetus to influenza diagnostic tests market share.

Some of the major trends that will influence the influenza diagnostic tests market are as follows:

Funding for influenza diagnosis, treatment and research boosting influenza diagnostic tests market growth

Influenza diagnostic tests market trends are changing commendably with increased government initiatives and funding. For instance, the government of South Australia started the 2019 Influenza Immunization Program, under which children with medical risk factors are eligible to receive a funded influenza vaccine, Fluarix Tetra®, for free.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/4242

An influenza protection company, Seqirus, recently filed an annual strain update with the FDA to manufacture Flucelvax Quadrivalent, their cell-based influenza vaccine, for the 2019-2020 flu season. The vaccine will use a cell based CVV (candidate vaccine virus) for four influenza strains identified by World Health Organization for the upcoming flu season. Moreover, a next generation infectious disease testing company also, recently received $21.9 million in a government funding, to develop breakthrough flu diagnostic technology.

Research programs are dynamically undertaken to improve human health. Various organizations are stepping forward with research on influenza. For instance, National Institute of Allergy and Infectious Disease has been conducting and supporting research to find improved ways to diagnose, treat and prevent influenza infection, which includes working towards innovating a universal flu vaccine that could provide enduring protection against multiple strains of influenza, such as those that cause seasonal flu as well as emerging forms capable of causing a global pandemic.

Growing prevalence of different types of influenza to expand influenza diagnostic tests market share

Increasing incidences of influenza across the world is driving the influenza diagnostic tests market growth. Among the different types of influenza, Influenza A and B are prevalent communicable respiratory diseases and are caused by infection with a virus, also known as bird flu or avian flu.

Type A can spread from animals to humans, while Type B is only contagious in humans. Types A and B can be equally severe and type C is a mild version of the influenza. In 2018, influenza diagnostic tests for Type A Flu was valued at $779.4 million.

RIDTs (Rapid Influenza Diagnostic Tests) detect influenza A and B viral nucleoprotein antigens in respiratory samplings and produce result in a qualitative format. RIDTs yield results in a clinically relevant time slot of less than 15 minutes. In the U.S., a number of RIDTs are commercially available. Growing adoption for flu diagnosing tests are expected to transform the influenza diagnostic tests market outlook over the forecast timeline.

Rising influenza frequency in the U.S. and rest of the world to boost influenza diagnostic tests market

Influenza annually affects 5%–10% of the population worldwide. Since influenza surveillance has been conducted for years in upper-income, temperate countries, this burden is well documented. Influenza being increasingly understood in middle-income countries and surveillance of the disease is substantially improving during recent years, leading to strengthening of influenza diagnostic tests market.

In the U.S., where influenza incidence is highly documented, The Centers for Disease and Control claims that between 15.4 million and 17.8 million people were affected by influenza in the 2019 flu season nationwide. The current flu season has been milder than last year’s, though there have been more deaths than usual from that milder strain. According to CDC, flu typically kills 12,000-56,000 people in the U.S., every year, which makes it much more crucial to detect and treat influenza on time.

Increasing prevalence of influenza in the U.S. will propel influenza diagnostic tests market growth in North America. Rising initiatives by the government to develop advanced technologies in order to deliver efficient results for influenza testing is another major factor that will escalate influenza diagnostic tests growth in the region. In 2018, the U.S. influenza diagnostic market was valued at $287 million and is further expected to witness substantial growth owing to presence of well-developed healthcare infrastructure, technological advancements and skilled professionals.

The World Health Organization, which keeps track of influenza cases and incidence around the world, has urged nations every year that while they enter the flu seasons, steps should be undertaken to strengthen case management, vaccination of high-risk groups and compliance with infection control measures. As diagnostic testing is a part of infection control, influenza diagnostic tests market is expected to gain momentum with industry size expected to surpass $1.5 billion by 2025.

Author Name : Aakriti Kakkar