Sustainable & Smart Technologies

Facilities management market to receive substantial gains from outsourced services segment by 2025

Stakeholders envisage facilities management market share to proliferate at a robust pace in the wake of unprecedented surge in smart city projects. Smart cities—integrated, powered and enabled by digital technologies—have propelled commercial spaces, transportation sector, namely. In recent years, awareness of facilities management has heightened owing to expanding tourism and hospitality industries.

Palpable surge in investments in construction and real estate is expected to underscore robust-looking facilities management market size. For instance, the Canadian government issued an additional funding of US$ 81.2 bn in 2017 across five main funding streams, including green infrastructure; public transit; social infrastructure; trade & transportation projects and meeting the ‘unique’ needs of rural and northern communities. Apparently, the unique needs include facilities to underpin food security, improved broadband connectivity and local access roads.

The Investing in Canada plan propounded in Budget 2016 and expanded on in Budget 2017, aims to build advanced economic cities. With burgeoning construction projects, demand for various services, including maintenance, construction, electric, operation and mechanical work has soared in recent times.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/4403

Facilities management market size is projected to surpass US$ 2 trillion by 2025, according to the latest research report by Global Market Insights, Inc.

Despite companies in the late 2000s focused on insourcing, of late there has been notable surge in outsourcing consumption. Companies tend to streamline their operations by embracing outsourcing that reduces business risks, expands profitability, grows competitiveness, enhances productivity and lets companies focus on their major business and competitive advantage.

As such, the outsourced services segment is slated to expand profoundly during the forecast period. That said, seemingly tepid adoption of outsourced FM services may dent the growth of the industry. Meanwhile, given that outsourcing apparently enhances operational efficiency, the outsourced services will underscore facilities management market size.

Popularity of smart homes and offices, including HVAC systems, fire safety systems, elevators, mechanical equipment has augured well for hard services segment that is set to hold significant share during the forecast period. As such, potential dominance of hard service segment is slated to bolster facilities management market share by 2025.

North America facilities management market is anticipated to expand robustly against the backdrop of proliferating tourism industry. With huge revenue at stake, governments globally are vying to woo would-be travelers to their countries led by aggressive marketing and favorable policies.

According to International Trade Administration (ITA), the U.S. travel and tourism industry garnered an economic output of over US$ 1.6 trillion in 2017. The dramatic upsurge witnessed in the number of tourists has been instrumental in rendering facilities management services across shopping malls, airports, amusement parks, and large food centers.

Leading companies are grappling to secure a government deal for FM services to augment their profitability and expand facilities management market size. In Q1 2019, Madrid City Government inked a four-year contract worth 18.62 mn with the facility management company ACCIONA. Reportedly, the Madrid City picked ACCIONA to enhance energy efficiency in 400 municipal buildings, including sports centers, schools, social and cultural centers, among others.

Author Name : Sunil Jha

Data warehousing market share to be propelled by statistical analysis segment over 2019-2025

Growing demand for effective ways of storage and testing of enterprise big data will help to augment data warehousing market size by 2025. Data warehousing is rapidly substituting conventional database management systems and legacy Business Intelligence (BI) tools. Data warehouses enable storage of disparate data by transmuting and standardizing several data types into one common format. Data warehousing helps to store large data volumes, and which can be retrieved faster in comparison to other operational systems. Huge benefits offered by the technology are offering impetus to the growth of data warehousing industry share.Data warehousing market forecast report predicts that on-premise data warehousing industry trends will be enhanced owing to low network latency and improved security. On-premise data warehouses do not undergo network lags and provide quicker query processing. These systems provide enterprises with improved data security because critical enterprise data is instituted on in-house data centers. Unification of other services is easier with on-premise data warehouse due to the presence of a single server.

Size of statistical analysis segment in data warehousing market is predicted to expand exponentially over 2019-2025. Statistical analysis comprises of compilation and analysis of quantitative data stored in a data warehouse, to discover fundamental statistical relationships. Statistical analysis tools have been observing a surge in demand owing to the adoption of these tools among government and research companies for past data analysis and to regulate helpful data patterns. Statistical analysis provides superior data re-usability (data recycling) for various sets of conditions. These conditions enable enterprises to create forecast models and predictive analysis algorithms by making minimal changes in data set.

Data warehousing industry forecast report has projected that manufacturing data warehousing market share will expand with a CAGR of more than 15% over 2019-2025. The growth is attributable to advent of Industry 4.0 and intensifying trend of cyber-physical systems in manufacturing facilities to generate huge data. Also, the advancements in manufacturing sector and increasing adoption of data warehousing technology will expand data warehousing market share significantly.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/3744

Huge investments are being made by manufacturing enterprises in IIoT and unifying data warehousing solutions with production management systems to plan for precise and data-driven manufacturing. For example, in February 2019, German automaker Daimler AG has reportedly deployed an in-house data warehouse known as eXtollo. This solution enabled Daimler to integrate IoT data with production planning systems. The integration helps to decrease material wastage, reduce production times, and cut down expense on product quality control. Demand for data warehousing is anticipated to escalate owing to efficient inventory planning and rapid production times in the manufacturing sector which will contribute to boost data warehousing industry outlook.

North America data warehousing market trends are projected to develop significantly by 2025 with a share of more than 40%. The growth can be accredited to strong ICT infrastructure, rapid adoption of cloud services, and augmenting prevalence of big data analytics. Companies in the region have been moving from traditional data warehouse tools to cloud-based solutions to raise scalability, cost-effectiveness, and to reduce hardware dependency. Presence of a number of key data warehouse vendors such as Oracle, IBM, Google, and Microsoft is also anticipated to drive North America data warehousing industry trends.

The main focus of the companies operating in data warehousing market have been on providing latest services and products to earn hefty revenue share. With the amplifying demand for data warehousing solutions, competitive landscape has been becoming more intense with major vendors have been focusing more on technology development and aggressive pricing to stay ahead of competition. A few of the key participants include IBM, AWS, Google, Oracle Corporation, Microsoft Corporation, etc. Reports predict that data warehousing industry size is slated to surpass $30 billion by 2025.

Author Name : Paroma Bhattacharya

4 major trends fostering global smart card market share

The payment card industry has introduced the EVM payment card method which has boosted the adoption of smart cards significantly. Increasing focus on security of organizations and user information has transformed smart card market outlook, with the advent of products capable of short-range wireless connectivity and can also be used as a token for multifactor authentication.

Described below are some factors influencing the demand for smart cards over the coming years:

- Increasing applications for hybrid cards

Hybrid cards will witness a steady adoption owing to multifunctional features and several smart applications that will conveniently contribute towards smart card market size. With rapid urbanization, certain countries have increasingly provided mass transportation for public travelling for greater efficiency and lower cost.

Hybrid chips are typically used for such mass transits that demand fast transaction time. Surge in security concerns in association with transactions and personal information will foster the demand for hybrid cards owing to the high level of security possible.

A hybrid card is also useful in accommodating the technology and infrastructure of a legacy system with the addition of e-card technologies in a single card. The product’s easy to use properties along with the high security provision will influence the product demand.

- Surge in use of microprocessors

Rising use of microprocessors in the banking and mobile phone sectors will contribute to the product growth. Microprocessors have their own operating system that is capable of processing data as a reaction at a given situation. The smart card is practical and a powerful tool due to its capability to record and modify information in its own physically protected and non-volatile memory.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/4312

Emerging markets like E-passports, assess control, PKI and other applications wherein the cryptographic abilities addresses the issues of security particularly demand microprocessor cards, expanding smart card industry scope.

- Growing telecommunication sector

Smart cards are secure elements and are widely used in the telecommunications industry around the world. These cards are used in two major applications like the prepaid telephone cards where the valued memory cards are stored as well as the Subscriber Identity Module (SIM), which are microprocessor based smart cards in mobile phones.

Moreover, smart cards are being used with NFC-enabled mobile phones that have incorporated secure elements and are being used for several applications that include ticketing, mobile marketing and other mobile contactless payments. This has tremendously bolstered global smart card market share from sim and telecom segment applications.

The smart card industry has UICCs and SIMs as the highest volume products for revenue and units. More than 100 countries use smart cards after having substituted coins in payphones in order to improve convenience for customers and telecommunication operators.

- Rise in daily consumer purchases

Increasing consumer needs and purchases will stimulate the applications of smart card in the retail & gas sector in the forthcoming years. The card can be used as electronic wallets while the chip has funds in order to pay for purchases like cafeteria food, taxi rides, groceries and laundry services. Bank connections are not required due to the cryptographic protocols that the money exchange between machine and smart cards have.

In an effort to save time and provide easy access of customer service to consumer, the government has been making efforts to use technology. India’s sole supplier of piped natural gas and CNG, Indraprastha Gas Ltd., recently launched prepaid smart cards in order to provide the customer with digital options for payment.

Key market players in the smart card industry like Oberthur, Inteligensa Group, CPI Card Group, American Banknote Corporation, IDEMIA, Perfect Plastic Printing Corporation, Watchdata, HENGBAO and Goldpac Group have introduced advanced smart solutions. Further collaborations and strategic acquisitions will influence the business outlook considerably. Global smart card market size is anticipated to surpass USD 65 billion by 2025.

Author Name : Riya Yadav

Top 3 trends driving assembly machine market forecast over 2019-2025

Manufacturing units across developing economies will be adopting Industry 4.0 technologies like artificial intelligence, machine learning and robotics to transform operations with the help of semi or fully-automated assembly machinery for achieving cost efficiencies without quality compromises.

Need for automatic and semi-automatic assembly machines

Semi-automated assembly machines will be witnessing a major growth in forthcoming years owing to a steady increase in the production of new and greener automobiles, that will in turn stimulate the demand for automotive components like radiators made on use semi-automatic assembly lines.

TQC Automation & Test Solution offers semi-automatic assembly machines in order to allow a manufacturer to test automotive radiators and enable quality control. Semi-automatic machines are essentially preferred over manual machines owing to the time saving functions. These machines are mostly used by small or medium enterprises for improving the manufacturing process under decent budget, while raising productivity and reducing the operational costs.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/4287

Fully automatic assembly machines will gain favorable traction and influence the business outlook due to use of smart technologies with the combination of cyber-physical systems that help factories become much more productive and energy-efficient. Automated assembly machines eliminate concerns for manual handling entirely and increases output in less time, fostering assembly machine market share globally.

Expansion of automobile and cosmetic manufacturing sectors

Major advances in the robotics technology have initiated the deployment of robotic automation in the automotive segment. Across automotive component plants, assembly machines comprising robots like high speed Delta machines help assemble small components such as motors and pumps. Car assembly involves windshield installation as well as wheel mounting that require automated assembling.

The European Union produced 19.2 million motor vehicles in 2018, which account for around 20% of the total motor vehicle production globally in the year. Companies in the region use advanced technologies for the manufacturing of automotive parts, considerably fueling Europe assembly machine industry size.

With regards to cosmetics packaging applications, equipment like pump priming and leakage testing machines, thin shape lipstick tube assembling machine, finish assembling machines and high-speed mascara bottling equipment run successfully in several multi-national companies. Several such automatic assembly machinery are imported by manufacturers based in Italy, United States, Switzerland and France that have helped the users to enhance their efficiency.

Surging consciousness among people about personal care and perception of beauty standards have increased the demand for cosmetics. Japan is one of the leading markets for beauty products and generated a revenue worth USD 36 billion in the year 2017.

Impact of growing demand in Asia Pacific region

Asia pacific region accounted for nearly 40% of global assembly machine market share in 2018, with countries like India and China reportedly looking to achieve lower manufacturing costs along with less technically skilled labor. Rapid digitization in the region has helped manufacturers expand and scale businesses economically.

Several countries have initiated Industry 4.0 projects for the improvement of manufacturing sectors, including Thailand, Malaysia and Indonesia, each having their own economic agendas.

Companies like Norwalt Design Inc., Hindustan Automation, FANUC Corporation, Kawasaki Heavy Industries Ltd, Humard Automation SA, Haumiller, Extol, Intec Automation and Bystronic Maschinen AG are some of the prominent equipment manufacturers comprising the competitive hierarchy of global assembly machine market.

Players are extensively involved in collaborations and look to acquire other companies to expand their portfolio. For instance, ABB had recently entered into a partnership with Cochin Shipyard, a government owned shipping corporation of India, to be able to provide automated assembly solutions.

Author Name : Riya Yadav

4 pivotal trends influencing global fraud detection and prevention market share

Fraud detection and prevention (FDP) market share is gaining immense momentum due to increasing cases of corporate economic theft and other financial crimes which lead to considerable revenue losses. Additionally, growing demand to track and secure real-time transactions is driving technological advancements in the field of digital payment, adding impetus to global fraud detection and prevention industry trends.Several government initiatives aim at securing online financial transactions carried out by the citizens and are spreading awareness about e-payment fraudulence along with levying stringent regulations.The burgeoning e-commerce sector is substantially driving the digital payments domain and providing opportunities to people involved in fraudulent activities. The e-commerce market in emerging countries is particularly ripe for the taking, with Indian e-commerce sector itself projected to surpass USD 120 billion by 2020. Rising penchant for online shopping and e-banking will certainly offer lucrative growth prospects for FDP industry.

Enumerated below is a summary of the top trends that are likely to be driving fraud detection and prevention market outlook over 2019-2025:

Increased deployment of fraud analytics

Growing number of cases of fraud in the banking, corporate, and e-commerce sectors is steering the demand for a reliable and accurate fraud detection systems in order to control the economic losses. Lately, fraud analytics has gained increasing demand as an effective FDP technology to help enterprises track or predict wrongdoings.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/1775

Fraud analytics comprises an amalgamation of analytic technology coupled with human interaction that assists in the detection of possible fraud or theft. Fraud analytics help in identifying hidden patterns, facilitate data integration, harness the unstructured data, enhance the existing efforts and facilitates real-time alerts and reporting, thereby making them an integral component of fraud detection and prevention market.

Application in credit and debit card frauds

Rising dependence on plastic money globally is intensifying the global FDP market scope. According to reports, as of 2016, the total value of card payments recorded in the U.S. was estimated at USD 5.96 trillion. In terms of numbers, credit cards segment had recorded a remarkable growth rate at 10.2% while debit cards grew by 6%. Evidently, there has been a rise in the adoption of credit and debit cards among people, raising the probability fraud.

There are several forms of credit and debit card frauds such as:

- Counterfeit card fraud

- Card ID theft

- Fake card

- Card Not Present (CNP) fraud

- Manual or electronic card imprints

The government and many key industry players are undertaking initiatives to spread awareness among the people regarding card usage and precautions that must be followed. The Reserve Bank of India, for instance has laid down guidelines to strengthen electronic banking transactions with an aim to facilitate customer protection. Growing demand for debit and credit cards has led to an increased adoption of fraud detection and prevention solutions.

Growing adoption in the banking sector

Increase in employment levels have led to a rise in disposable incomes worldwide, propelling the banking industry globally. Banking sector is witnessing rising demand for online services and credit cards in Asian countries like Japan, China, India, among others, owing to the rise in industrialization and globalization.

As per reports, for the fiscal year 2017-18, the total bank deposits in India increased at a notable CAGR of 11.66% and was slated to increase rapidly in the forthcoming years. Rising demand for a robust digital banking infrastructure has given rise to technological innovations such as IMPS, NEFT, mobile banking and other forms of digital payment methods.

Suring bank fraudulence in terms of check tampering, credit and debit card fraud cases, cash transaction monitoring and incorrect accounts keeping may lead to huge economic losses to countries. A burgeoning banking sector will undoubtedly complement the global fraud detection and prevention industry forecast.

Financial market trends in North America

While the demand for FDP services has been rising across several regions such as Europe, MEA and APAC, North America is likely to emerge as one of the more profitable revenue terrains for fraud detection and prevention industry share.

The financial and insurance sector in the U.S. was valued at USD 1.5 trillion and represents one of the most liquid financial markets in the world.

The robust financial sector in North America is experiencing increasing attempts at financial frauds and thefts. Reportedly, over 74% of the financial institutions based in North America have reported online or mobile fraud losses. It was estimated that by 2022, the financial organizations would spend over USD 9.3 billion annually on tools for fraud detection and prevention.

The presence of global financial multinationals as well as leading security service providers in North America will significantly amplify fraud detection and prevention industry size in the years ahead.

Author Name : Shreshtha Dhatrak

3 key trends fostering global bike sharing market outlook

Rising environmental concerns along with the implementation of government regulation will outline bike sharing market trends over the forecast period. Rapid modernization and urbanization has caused major traffic problems that has been associated with safety risks, air pollution, economic competitiveness, loss in relation with accessibility and sustainable growth.Bike sharing schemes offer transport flexibility, reduced congestion as well as fuel congestion and reduction in harmful emissions.

Increasing health consciousness among people owing to the rise in health conditions as a result of living a sedentary lifestyle will contribute towards expanding bike sharing industry share. Bikes play a major role in leading a healthy lifestyle and exhibit some key health benefits. The benefits of biking comprises flexible joints, stronger bones, lower body fat levels, improved cardiovascular fitness as well as reduced anxiety and stress levels.

Rapid advancements in technology has led service providers to install appropriate navigations systems in bicycles which helps people find their destination. The convenience delivered by the improving technology will foster bike sharing market size. Copenhagen had launched an efficient and innovative bike sharing program a few years ago that was offering GPS-enabled Android tablets with the bikes.

The new equipment was to help commuters schedule their travel by train or bike and ensure that they are aware of their new pick up connection.

Listed below are few trends that will likely fuel global bike sharing industry forecast:

- Rising investments into startups

Key venture investments have been proliferating the growth of bike sharing market because of a large number of capitalists steadily investing in bike sharing start-ups in order to help them grow. Funding has recently taken off around the world and has been considered ideal for the first and the last mile transport. This has resulted in investors placing their bets on bike sharing companies. Companies in China that have already established their presence in the market have attracted significant investments.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/4302

Ofo, for instance, became the first bike sharing unicorn in China and scaled globally, showing clear potential to secure additional investments. The company was valued at $3 billion and has raised more than USD 2.15 billion in its series of funding by companies like Ant Financial and Alibaba. In the follow-on of Series E round, Ofo raised USD 586 million in March 2018 in order to fund its global expansion.

Hellobike, the third largest bike sharing platform in China had also raised an investment of USD 321 million from Ant Financial and has been trailing behind companies like Ofo and Mobike.

- Emerging E-bike sector

E-bike has been gaining a momentum due to an increase in the adoption of smart bikes. Key merits attached to this service is that it permits dockless operations which entails a light infrastructure at a much lower cost. Consumer preference towards E-bikes have been surging due to its cost effective features coupled with solutions that are eco-friendly, driving the expansion of bike-sharing market size.

PBSC Urban Solutions along with BIXI Montreal recently teamed up to offer next-gen E-FIT bikes that will seamlessly fit into the public bike systems. The bikes are lightweight and offer three-speeds for maximum rideability. After the combination with PBSC’s E-station, the integrated batteries start charging right after the bikes are docked which has increased daily trips over 15%.

- Affordability of free floating bikes

Free Floating bike sharing segment will witness a considerable growth over the analysis period owing to its affordability. Dockless bike share will reduce the cost of buildings or stations used for bike parking which in turn will help increase its deployment. Consumer inclination towards this segment will increase due to the convenience of parking bikes anywhere at their stop. The navigation system installed in these bikes help find their locations and can be unlocked through bike sharing apps.

The Ministry of Transport says that China has nearly 70 companies that have deployed over 23 million bicycles nationwide and have attracted more than 400 million users. With a revenue of $35 billion, this industry has helped create over 390,000 jobs. It has also been estimated that dockless bike sharing in China has helped reduce 400 million hours of time spent in the traffic. This has established a low-carbon network for transport and lessened the pressure for urban transport.

Major companies underscoring global bike sharing market forecast including Neutron Holdings Inc., Tembici, Divvy Bikes, Capital Bikeshare, Lime, Youon Bikes and Mobike. The players have consistently involved in gathering investments and collaborating with firms and governments for the expansion of their business.

Author Name : Riya Yadav

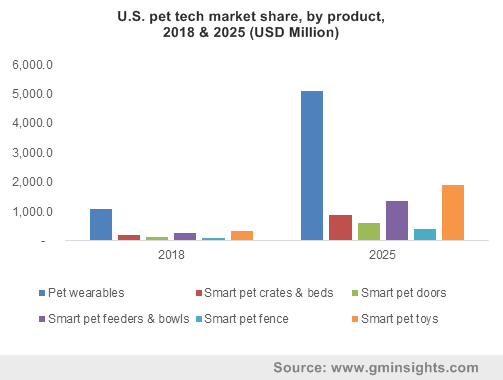

Pet tech market trends to be driven by rising innovations brought forth by industry players

Pet tech market trends are anticipated to depict a rapid transformation owing to the rising prevalence of pet e-commerce and advent of products with tech enabled services that lead to the pets’ enhanced wellbeing and security. Nowadays pet owners are looking for novel approaches to keep their pet happy and healthy which would further substantially influence pet tech market outlook over the forecast period.

U.S. pet tech market share, by product, 2018 & 2025 (USD Million)

Prominent reports suggest that in recent years, the annual spending on pets has surged to double due to the busy schedule of pet owners. As companies continue to offer top-grade products like high-tech fences, pet cameras, automatic food bowls, and more, pet tech industry size is expected to substantially increase in the ensuing years.

Pet technology has become a rapidly emerging market remnant of electronic and connected solutions which help owners to train, monitor, feed, and play with their furry friends. According to studies, security and safety are considered as major concerns for the pet owners and most of them opine that technology will help resolve them efficiently. Pet tech manufacturers are looking to develop new products and advanced solutions for pets that will help attract a significant consumer pool comprising pet lovers. This would further enhance the growth of pet tech market share in the upcoming years.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/4187

Of late, companies have been working to launch novel products like smart cameras that are designed to be the perfect assistants for busy pet parents through which they can talk, watch and even play with their pets remotely. The pet owners can receive notifications about their pet’s behavior and can undertake continuous home monitoring. Such products brought forth by industry players will considerably contribute to stimulate pet tech industry trends.

In terms of the regional landscape, the North America pet tech market held more than 55% of the industry share in 2018 and will experience steady growth due to the increase in the adoption of technological solutions in the household sector. It has been observed that major changes in pet ownership are in the pipeline due to the advent of technological and cultural change.

Nowadays, pet parents are opting, not for traditional food but nutritious food with healthy ingredients for their pets. They are also paying more attention to pet care, grooming, transportation, and many other aspects. The pet owners in North America are spending massively on the health and fitness of their pets as well.

In 2017, it was projected that the mutual gross written premiums of pet health insurance were registered at more than USD 1.2 billion. The household pet ownership in the region is witnessing high growth, which stimulates pet care companies to manufacture more tech-enabled products, in turn, propelling the pet tech industry share.

Pet tech companies are on the continuous quest of undertaking novel methods to keep pets close to their owners which has given rise to several new applications and solutions that can make the pet’s life feasible and trouble-free. For instance, in May 2019, Petz, a chain of pet shops in Brazil had recently created an e-commerce tool named Pet-Commerce which combines artificial intelligence with facial recognition to aid dogs make their own online shopping decisions and provide their dogs the best- ever experience. These novel innovations will attract more pet owners and highlight the substantial growth potential for pet tech industry players.

Considering the efforts undertaken by the remarkably industry players, it is clear that the pet tech market would depict substantial growth in the forthcoming years. The competitive spectrum of this industry is distinctive and consists of renowned companies such as Fitbark, IceRobotics, Garmin Ltd., Konectera, Whistle Labs LLC, Loc8tor, Motorola, Nedap N.V., Pod Trackers Pty Ltd, Tractive, Petcube, Inc., Petnet Inc., Scollar, PetPace LLC, CleverPet, Petrics, and WOPET.

Exemplary initiatives by the leading players will undoubtedly have a lasting impact on the growth prospects of this industry. Global Market Insights, Inc. estimates that pet tech market size will exceed the USD 20 billion mark by 2025.

Author Name : Deeksha Pant

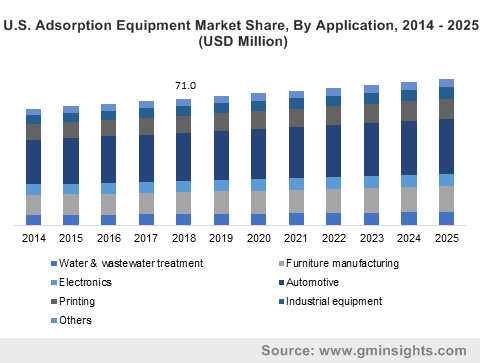

Growing automobile sector to bolster adsorption equipment market forecast over 2019-2025

Increasing awareness with respect to volatile organic compound emission (VOC) has propelled adsorption equipment market share, along with the need to maintain indoor air quality standards across varied industrial segments. Symptoms of nausea, difficulty in breathing, irritation in nose, eyes and throat are some of the indicators of excess exposure to VOC caused to humans. These conditions can usually be observed in manufacturing, printing and furniture operations worldwide, presenting a massive need for countering these emissions.

U.S. Adsorption Equipment Market Share, By Application, 2014 – 2025 (USD Million)

Booming automobile sector across developed and developing nations has strengthened the adsorption industry size. Paints used in the automotive industry emit high levels of xylene, acetic acid, butyl ester and ethyl acetate either during intermediate, top coating and baking process of automobile parts. The growing automobile industry in India, which had witnessed a 9.5% increase in sales to reach 4.02 million units in the year 2017. Widespread application across the auto manufacturing sector will evidently create a substantial demand for controlling VOC emission from paints, magnifying global adsorption equipment industry outlook.

Disposable or rechargeable canisters segment accounts for a substantial share of adsorption equipment utilized worldwide, and is expected to surpass USD 65 million in revenues over the forecast period. These canisters are widely used in the water purification process. According to a report by United Nations, by 2030 over 700 million people globally could be displaced owing to intense water scarcity.

Existence of water pollution in terms of organic pollutants let out by domestic sewage, agricultural wastewater and industrial wastes has added to increase in toxic waste in water. Toxic pollutants can lead to severe environmental issues and can prove to be extremely hazardous to living beings. Adsorption equipment market size will expand notably while becoming an integral part of wastewater management techniques.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/4206

R&D in the field of vapor adsorption equipment has enhanced the overall industry scope remarkably. For instance, the development of Brayton cycle heat pump that facilitates VOC recycling and recovery has magnified the deployment of adsorption equipment, invariably driving the industry trends. Vapor phase segment in adsorption equipment industry is anticipated to hold a significant share, registering a steady CAGR of around 2.5% from 2019 to 2025.

Owing to the rising automobile sector coupled with stringent regulations related to VOC emissions. the use of adsorbers in the automotive sector has accelerated. Reportedly, the gross turnover generated by the auto sector in EU represents 7% of its GDP. Moreover, governments have introduced an Integrated Pollution Prevention and Control Directive (IPPC) that requires all new installations to comply with its standards in order to control air, water and environmental pollution. The proliferation of automobile, electronics, water treatment and printing sectors in the region will positive steer Europe adsorption equipment market outlook.

Demand for adsorption equipment is clearly driven by the growing need for industries to preserve environmental, water and air quality. With expanding industrial establishments across the globe, governments and other regulatory authorities are discovering the need to control the VOC emissions in order to protect the future of economies. Simultaneously, increasing innovations in the adsorption equipment sphere to suited varied industrial applications is providing impetus to global adsorption equipment industry.

Emissions are an inevitable part of many crucial sectors such as automobile, painting, printing, water treatment, among others, in order to adhere to the government rules and regulations and to contribute to the growing CSR activities by the companies. Several key players offering critical adsorption equipment include Tigg LLC, Monroe Environmental Corp, Munters Corporation and Eisenmann SE, as well as several others. Global Market Insights Inc. has estimated that global adsorption equipment market share will exceed annual valuations of USD 340 million by 2025.

Author Name : Shreshtha Dhatrak

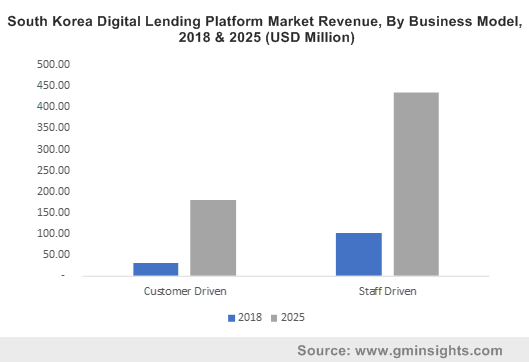

Rising inclination toward digital transformation to drive digital lending platform market trends

Growing adoption of mobile banking services driven by rapid digitization trends has fueled digital lending platform market size over the past few years. Consumer inclination towards using digital lenders for automotive loans is growing steadily owing to minimal documentation required, transparent and quick loan processing, as well as lower interest rates compared to conventional lending. Increasing implementation of software solutions among financial institutions to reduce operating costs and deliver services via digital channels is anticipated to bolster product demand worldwide.

South Korea Digital Lending Platform Market Revenue, By Business Model, 2018 & 2025 (USD Million)

A digital lending platform will essentially reduce operational, business as well as regulatory risks in digital lending organizations with a responsive and configurable approach. Use of digital platforms will cater to the mounting demand among financial organizations for enhanced customer experience while interacting with lenders and borrowers, providing speed and transparency. These platforms also improve loan collection and repayment methods for institutions with efficient real-time loan approval, processing and disbursal, which will augment digital lending platform industry share over the forecast period.

Studies have estimated that 53% of adults worldwide will be using smartphones, PCs, tablets or smartwatches to avail financial services by 2021. Cloud-based digital lending platforms are already being used by banks and NBFCs to reach customers across the globe, informing them about the status of their loan payments as well as basic account information.

Get a Sample Copy of this Report:@ https://www.gminsights.com/request-sample/detail/3019

A large number of banks are leveraging the opportunity to offer digital lending services for expanding their customer base, impacting product demand. Moreover, expansion of IoT coupled with the cloud computing revolution in digital banking will help meet customer expectations by redefining loan processes, strengthening digital lending platform market outlook.

Technology has been the driving force in business transformation over the years, but the speed at which advanced technologies are being launched has reached an unprecedented level. Increasing digitalization worldwide along with growing adoption of digital platforms for conducting business is anticipated to stimulate digital lending platform industry prospects.

Digital transformation is not solely based on development of new technology, but also an organization’s ability to accept transformation at the intersection of business and people. Reportedly, 55% of startups had already switched to digital business strategies in 2018 as opposed to 38% of conventional organizations. This suggests that startups will be accountable for increasing revenue via digital platforms, expanding the scope of digital lending platform market.

Built Technologies, which focuses on taking construction lending into the digital age, had raised close to $21 million in a Series A round in 2017. The company was aimed at using digital transformation to enable lenders to use data for making more informed decisions on their loans while simultaneously providing borrowers a conveniently digital user experience with quicker access to money and propelling projects forward. Rising adoption of digital technology for lending among financial companies for loan repayments is expected to complement digital lending platform industry trends over the forecast timeframe.

Increased utilization of internet services coupled with changing end-user requirements are encouraging financial organizations to shift to digital business models for managing consumer needs on their choice of channel. Advent of advanced technologies such as biometric-based authentication, e-signatures, e-mandates, ML, AI, advanced analytics and blockchain for mitigating fraud and NPAs risk is estimated to bolster digital lending platform market expansion.

Declining costs of internet connectivity and fast-paced advancement in smartphone technology will support the rising digitalization across financial institutions, proving to be crucial factors in pushing the market growth.

Leading market players are relying on strategic alliances through mergers and acquisitions to enhance product offerings and expand their regional presence. Key players comprising digital lending platform space are Built Technologies, Finastra, Finantix, Nucleus Software, Arena Limited and Newgen Software Technologies Limited, among several others. Global digital lending platform market size is projected to surpass USD 17 billion in annual revenues by 2025.

Author Name : Hrishikesh Kadam